Medical Debt Is a Manufactured Crisis Decades in the Making

By MHB Admin ·

No other wealthy country produces medical debt at industrial scale. People get sick everywhere; only in the United States does illness routinely convert into a collections account, a court judgment, or a garnished paycheck. That difference is the first clue that medical debt is not a natural disaster. It is an output — the predictable product of decisions about how care is priced, how insurance is designed, and how unpaid bills are monetized. Each of those decisions has beneficiaries, and none of them is the patient.

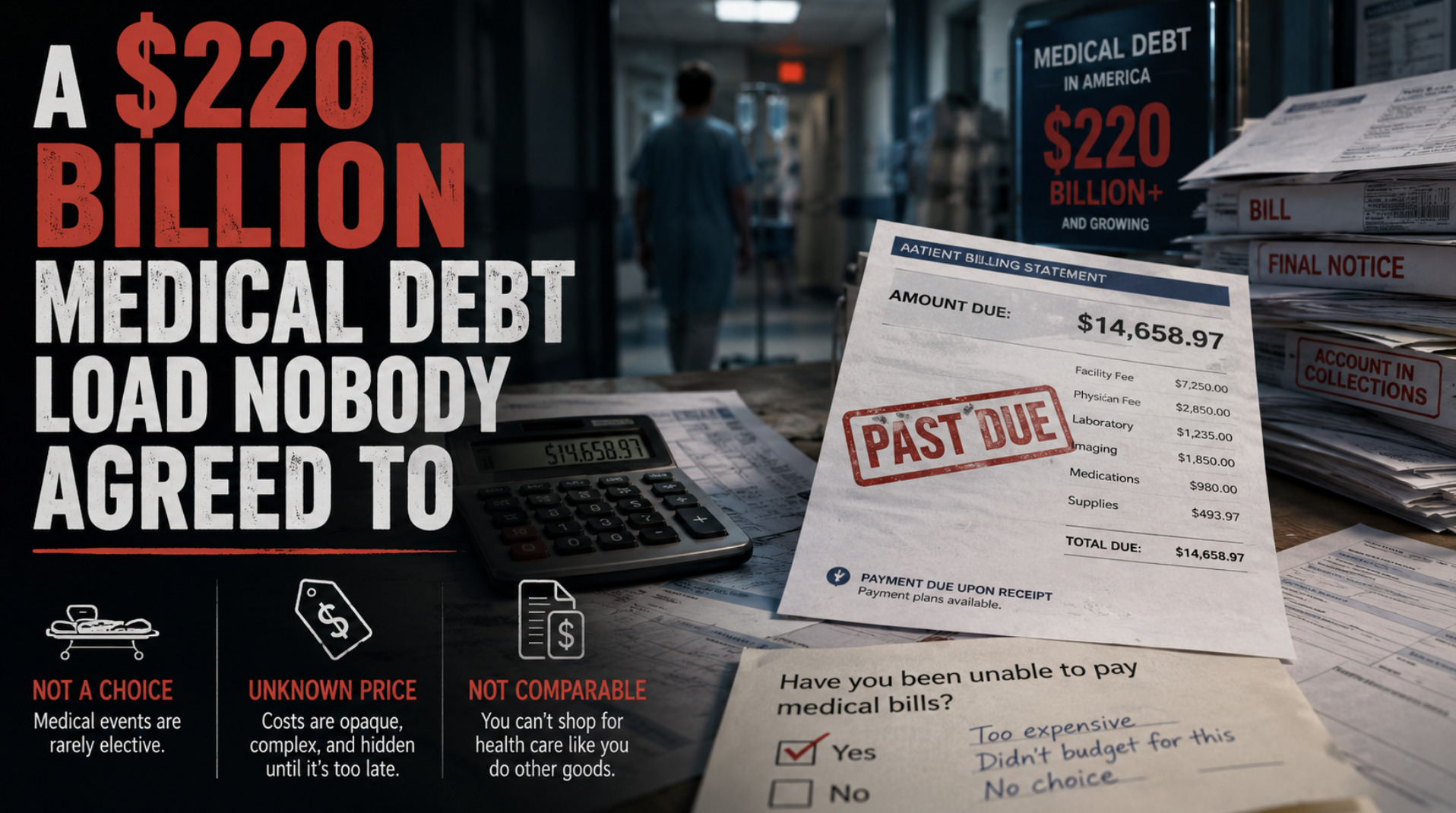

The scale is hard to absorb. Americans owe at least $220 billion in medical debt, according to the Peterson-KFF Health System Tracker. Roughly 14 million people owe more than $1,000; about 3 million owe more than $10,000. And those figures use a narrow definition. When KFF's survey researchers asked about all debt taken on because of medical or dental bills — credit cards, payment plans, loans from family — 41 percent of American adults reported carrying some, a figure the KFF Health News "Diagnosis: Debt" investigation translated into roughly 100 million people. This is not a fringe problem afflicting the uninsured. Most people with medical debt had insurance when the debt was created.

A $220 Billion Medical Debt Load Nobody Agreed To

Consumer debt usually begins with a choice. A mortgage, a car loan, even a credit card balance reflects a decision to buy something at a known price. Medical debt inverts every part of that logic. The "purchase" is often involuntary — an appendix does not negotiate. The price is almost never known in advance, and frequently is not knowable even in principle, because it depends on a lattice of chargemaster rates, network discounts, and coverage determinations that resolve weeks after treatment.

This is why economists treat medical debt as categorically different from other consumer debt, and why the Consumer Financial Protection Bureau found in 2022 that medical bills accounted for more than half of all collections tradelines on consumer credit reports — roughly $88 billion at the time. People do not budget their way into medical debt, and they cannot shop their way out of it.

Deductibles Did the Quiet Work of Shifting Costs to Patients

The crisis grew fastest not among the uninsured but among the insured, and the mechanism was the deductible. Over the past two decades, employers and insurers responded to rising premiums by shifting costs onto workers: deductibles for employer coverage rose far faster than wages, and high-deductible plans went from a niche product to a default option. The theory was that patients with "skin in the game" would become careful shoppers and discipline prices.

The theory failed on its own terms — patients cut back on necessary and unnecessary care alike, and prices kept rising — but it succeeded brilliantly as a cost transfer. A family with employer insurance and a deductible of several thousand dollars is, for practical purposes, uninsured for the first several thousand dollars of any bad year. KFF's survey work shows the result: about a quarter of adults report medical or dental bills that are past due or that they cannot pay. The insurance card in their wallet did not prevent the debt; it structured it.

The Chargemaster Economy Behind Every Inflated Bill

Upstream of every collections call is a price that bears little relation to cost. Hospital chargemasters — the internal master lists of prices — function as opening bids in negotiations with insurers, inflated precisely so that discounts can be granted from them. The people most likely to be billed at or near chargemaster rates are those with the least market power: the uninsured and the out-of-network, who receive the list price that no insurer would ever pay.

Federal price transparency rules now require hospitals to post their negotiated rates, and compliance has been uneven since the requirement took effect. But transparency, even where it exists, does not help someone arriving by ambulance. The pricing system was built for negotiations between institutions, and patients are simply the parties who absorb its residue. It is the same structural pattern this site has traced in other systems: opacity is not a bug of the machine but the condition that lets it keep running.

Nonprofit Hospitals That Collect More Than They Give

Roughly half of U.S. hospitals are nonprofits, exempt from most federal, state, and local taxes on the premise that they provide community benefit — above all, free or discounted "charity care" for patients who cannot pay. The Congressional Research Service has outlined how loosely that bargain is enforced: federal law requires nonprofit hospitals to maintain a financial assistance policy, but sets no minimum amount of charity care.

The results are what one would expect from an unenforced bargain. One study estimated nonprofit hospitals' tax exemptions were worth over $28 billion in 2020; a 2023 analysis of more than 1,700 nonprofit hospitals found that 77 percent spent less on charity care and community investment than the estimated value of their tax breaks. A New York Times investigation found that Providence, one of the country's largest nonprofit systems, trained staff to press payment from patients who qualified for free care under its own policy, while its charity-care spending hovered near 1 percent of operating expenses. A bipartisan group of senators, led by Chuck Grassley and Elizabeth Warren, has asked the IRS and its inspector general to examine whether the sector is honoring its tax-exempt obligations at all; Grassley's earlier oversight of a Missouri nonprofit hospital that sued patients eligible for charity care produced $16.9 million in debt forgiveness for more than 3,000 people.

The pattern deserves plain language: institutions are collecting a public subsidy for generosity while running collections operations against the people the subsidy was meant to protect.

Courts and Credit Bureaus as the Collections Back Office

Unpaid bills become an asset class the moment they leave the hospital. Debt is worked in-house, placed with collection agencies, or sold for pennies on the dollar to buyers who then pursue the full face value. The enforcement arms of this industry are public institutions. Research published in JAMA has documented nonprofit hospitals suing low-income patients and garnishing their wages, and studies of hospital litigation have found that roughly a quarter of hospitals have sued patients in recent years — often over amounts of a few thousand dollars or less, and often targeting people who work for low-wage employers. Most states allow wage garnishment for medical judgments; only a handful prohibit it. Small-claims dockets in some counties are dominated by medical creditors, courts functioning as a subsidized back office for the industry — a use of public legal machinery against poor defendants that will be familiar to readers of our reporting on civil forfeiture.

Credit reporting supplies the other lever. In January 2025 the CFPB finalized a rule removing medical bills from credit reports entirely, on the evidence that medical collections are poor predictors of creditworthiness. In July 2025, a federal judge in Texas vacated the rule, holding that the bureau had exceeded its authority — and that federal law preempts state attempts to impose similar protections. What survives are the credit bureaus' voluntary concessions from 2022 and 2023: paid medical collections and debts under $500 no longer appear, and new medical collections wait a year before reporting. Voluntary concessions, by definition, can be withdrawn.

Who Profits When Sick People Owe

A crisis persists when enough parties are paid by its persistence. Hospitals use aggressive collections to defend revenue and list prices to anchor negotiations. Insurers use deductibles to hold premiums presentable while transferring risk to members. Debt buyers purchase receivables at steep discounts and profit from whatever the courts help them extract. Financing companies now sit inside hospital billing departments, converting bills into medical credit cards and loans that carry interest the original bill never did. Each actor behaves rationally; the aggregate is 100 million people in debt for having bodies.

The commonly proposed fixes track the diagnosis. Enforceable charity-care minimums would put terms on the nonprofit bargain. Screening patients for assistance eligibility before any collections activity — arguably already implied by federal 501(r) requirements — would catch the Providence pattern early. Several states and localities have begun buying and retiring medical debt in bulk, which relieves individuals but, as its own advocates concede, does nothing to slow the machine producing new debt behind it.

The Manufactured Part Is the Point

Calling medical debt a manufactured crisis is not rhetoric; it is a description of the supply chain. Prices set in institutional negotiations, insurance designed to shift costs downward, a legal system that enforces the resulting paper, and a tax code that subsidizes the collectors — remove any one of these design choices and the output shrinks. Other countries made different choices and do not have the product. The debt is not evidence that Americans consume health care irresponsibly. It is evidence that a system has learned to convert illness into receivables, and that the conversion has been profitable enough, for enough parties, to protect itself for decades.